Northern Ireland’s beef trade is showing clear signs of pressure this spring, with the latest market evidence pointing to a softer tone in prime cattle prices even though local slaughterings remain below last year’s level.

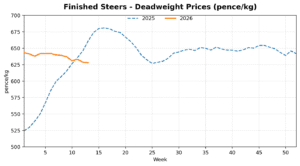

UFU analysis of LMC-based Price Watch data shows that factory quotes have eased from around 630–640p/kg in early January to 600–610p/kg in recent weeks, a fall of roughly 20–30p/kg or 3.1% to 4.8%.

The latest DAERA Agricultural Market Report for the week ending 4 April 2026 also reflected that weaker tone. The report recorded all-grades average prices of 627.9p/kg for steers, 629.0p/kg for heifers and 608.5p/kg for young bulls, while the average cow price stood at 498.9p/kg.

At first glance, tighter local numbers might have been expected to offer more support. However, the LMC analysis shows that while NI prime cattle slaughterings were down from 57,086 head in 2025 to 54,748 head in 2026 by late February, average prime carcase weights rose from 337.7kg to 350.7kg. Heavier cattle almost fully offset the lower throughput, meaning total beef production fell by only 0.4% despite a 4.1% drop in slaughter numbers.

That is important for finishers. Fewer cattle are coming forward, but each animal is producing more beef, so the reduction in available supply is not as sharp as slaughter numbers alone might suggest.

Imports are also influencing the market. Imports from the Republic of Ireland for direct slaughter were running 4.3% above the same period last year by early April. At the same time, wider UK import growth from countries such as Australia, New Zealand and Brazil has added pressure across both the UK and Irish beef markets.

This does not mean imported beef is directly displacing NI product in every case, but it does mean processors and retailers have more supply options in the background, weakening the extent to which tighter local supplies can lift farmgate prices.

Consumer resistance is another part of the picture. AHDB retail data shows beef spend rose 8.8% over 12 weeks, but that increase was entirely price-driven, with volumes back 6.5%. Primary beef volumes fell 9.1% and processed beef volumes were down 6.8%. Consumers are still buying beef, but less of it as prices rise in shops, making retailers and processors more reluctant to keep pushing farmgate prices upwards.

Processor control over throughput also remains a factor. In ROI, Agriland reported processors were reducing kill days and managing lower overall cattle availability. That is not NI-specific proof, but it matters because the NI and ROI markets are closely linked. In the week ending 4 April, GB steer prices averaged 636.1p/kg versus 627.9p/kg in NI, while GB heifers averaged 633.8p/kg against 629.0p/kg in NI. That suggests tighter local supplies are not automatically being passed back to NI finishers through stronger competition.

For beef finishers, the real concern is margin. Irish Farmers Journal analysis suggested losses of around £200 per head this spring. The example was based on a 550kg continental steer bought last autumn at 400p/kg, or £2,200 per head. At current returns, the animal might generate around £2,570, but once costs are included the average margin still comes out at a loss of about £196 per head. This does not account for poor performance or mortality, and even with support payments margins remain tight. Earlier store prices mean many finishers would have needed over 700p/kg to break even, while actual prices have been closer to 642–644p/kg.

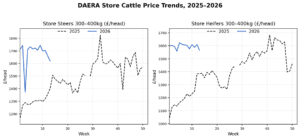

DAERA store cattle charts also underline that pressure. Average prices for 300–400kg steers and heifers were running well above 2025 levels in the opening weeks of 2026, meaning many finishers were buying replacement cattle at elevated values even as finished returns softened.

Additional commentary from Ireland points in the same direction. Francie Gorman of the IFA said on 31 March that cattle finishers were looking at losses of €300 to €400 per head on cattle bought last October. Teagasc has also indicated that a winter finisher could face an average loss of €512 per head, although that is best treated as a supporting indicator rather than a lead figure.

Overall, the message is clear, local beef supplies may be tighter in headcount terms, but heavier carcases, increased imports, weaker retail demand and processor control over throughput are all limiting price support. For Northern Ireland beef finishers, that means the pressure on margins remains very real.

Related Stories

UFU beef campaign highlights need for urgent action on imports and labelling

UFU urges FSA to maintain vital support for NI meat sector